For many, budgeting is a relentless monthly cycle of tracking bills and hoping there’s money left over. But what happens when the inevitable large, non-monthly expense arrives—like annual car insurance, holiday gifts, or a dream vacation?

These planned but infrequent costs often derail even the most disciplined monthly budget, leading to debt or panic.

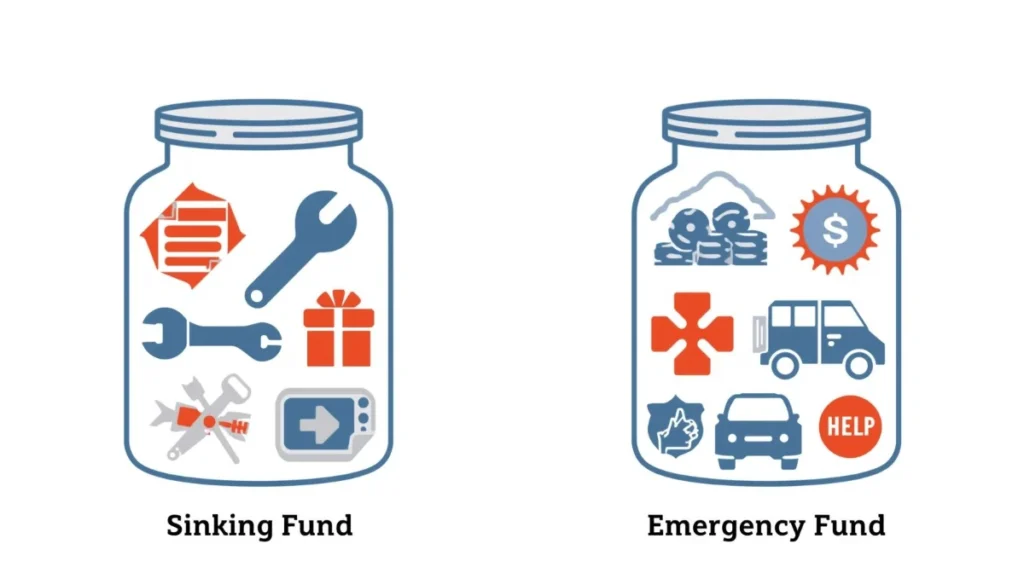

The solution is the Sinking Fund.

A Sinking Fund is not an Emergency Fund. While an Emergency Fund is for unforeseen disasters (loss of a job, medical emergency), a Sinking Fund is specifically for anticipated, irregular expenses.

By breaking down large future costs into manageable monthly savings goals, you can budget for these expenses proactively, ensuring financial predictability and peace of mind.

This comprehensive guide will walk you through the five simple steps required to set up and successfully manage your Sinking Funds, turning large financial hurdles into small, consistent contributions.

I. What Exactly is a Sinking Fund?

A. The Difference Between Sinking Funds and Emergency Funds

Understanding the distinction is key to financial success:

| Feature | Sinking Fund | Emergency Fund |

| Purpose | Saving for known, future expenses (e.g., insurance, travel). | Saving for unexpected financial disasters (e.g., job loss, injury). |

| Liquidity | Highly liquid; funds are spent when the due date arrives. | Reserved; funds should only be used in true financial emergencies. |

| Funding Goal | Specific target amount based on the expense (e.g., ₹50,000 for a trip). | Broad target (e.g., 3 to 6 months of living expenses). |

Sinking Funds allow you to treat large, annual or sporadic costs as fixed, predictable monthly expenses within your budget.

II. Step 1: Identify and Quantify Your True Expenses

The first step in creating a Sinking Fund budget is to perform a thorough audit of all your irregular expenses.

A. Common Sinking Fund Categories

Go beyond your monthly bills and list every expense that hits your bank account annually or semi-annually:

- Annual/Semi-Annual Bills: Car insurance premium, property tax, software subscriptions, professional licenses, annual membership fees.

- Expected Replacements: Car replacement (down payment), furniture replacement, home appliance repair/replacement fund.

- Holidays & Gifts: Birthday gifts, holiday shopping (Diwali, Christmas), annual vacations.

- Personal Maintenance: Annual health checkups, dental cleanings, pet care costs (annual vaccination).

B. Determining the Exact Financial Goal

Once you have the list, calculate the exact amount of money you will need for each expense and when it is due.

- Example 1 (Fixed Cost): Car Insurance Premium is ₹30,000, due in 6 months.

- Example 2 (Estimated Cost): You want to spend ₹1,20,000 on a vacation next year (12 months).

- Example 3 (Replacement Cost): You estimate a new laptop will cost ₹60,000 in 24 months.

III. Step 2: The Critical Calculation (Divide and Conquer)

This is the most crucial step. You must calculate the exact monthly contribution required for each fund.

A. The Sinking Fund Formula

The formula is simple, but powerful:

$$\text{Monthly Contribution} = \frac{\text{Total Cost of Expense}}{\text{Number of Months Until Due}}$$

B. Calculating Monthly Targets

| Expense | Total Cost | Months Until Due | Monthly Contribution |

| Car Insurance | ₹30,000 | 6 Months | {₹}30,000 / 6 ={₹}5,000 |

| Vacation Fund | ₹1,20,000 | 12 Months | {₹}1,20,000 / 12 = {₹}10,000 |

| New Laptop | ₹60,000 | 24 Months | {₹}60,000 / 24 ={₹}2,500 |

| Total Monthly Sinking Fund Obligation | – | – | ₹17,500 |

This total amount (₹17,500 in the example) is now a Fixed Expense in your monthly budget. You budget for this before any discretionary spending.

IV. Step 3: Integrate and Automate the Transfers

A Sinking Fund works only if the money is actually saved and protected from day-to-day spending.

A. Budget Integration: Treating it as a Bill

In your Zero-Based Budget (or any budget), the total monthly Sinking Fund obligation must be treated with the same severity as rent or minimum debt payments. When you do your monthly allocation, the ₹17,500 goes to Sinking Funds immediately.

B. The Power of Automation

The simplest way to ensure consistency is to set up an automatic monthly transfer.

- Action: Set up recurring transfers from your primary checking account to your dedicated Sinking Fund Savings Account (see Step 4) immediately after your paycheck hits.

- Frequency: Align the transfer date with your regular income deposits (e.g., 1st or 15th of the month).

C. The “Roll With the Punches” Rule

If you have a low-income month (relevant for freelancers), you may need to reduce a discretionary Sinking Fund contribution (like the Vacation Fund). However, never reduce contributions to essential Sinking Funds (like the Annual Insurance Fund) unless absolutely unavoidable.

V. Step 4: Setting Up the Accounts (The Digital Envelope System)

The money saved for Sinking Funds must be kept safe but liquid. It should not be mixed with your general savings or emergency fund.

A. Separate Savings Account Strategy

The ideal strategy is to open one or more separate, dedicated High-Yield Savings Accounts (HYSAs).

- Option 1: The Single Bucket: Use one HYSA and track the individual fund balances inside the account using a simple spreadsheet or a dedicated budgeting app (like YNAB).

- Option 2: Multiple Buckets: Open multiple HYSAs (many banks allow several sub-accounts) and label them clearly (e.g., “Sinking Fund – Car Insurance,” “Sinking Fund – Vacation”). This provides clear visual separation and prevents accidental overspending from one category.

B. Why an HYSA?

Sinking Fund money should earn interest but must remain easily accessible. HYSAs offer better returns than standard checking accounts while keeping the funds liquid, as they are meant to be spent.

VI. Step 5: Spending and Replenishment

A Sinking Fund is designed to be spent! This step is about successfully deploying the money and preparing for the next cycle.

A. The Painless Payment

When the expense due date arrives (e.g., the car insurance bill), you transfer the exact amount from the relevant Sinking Fund account to your checking account and pay the bill. The key difference here is that the money is already accounted for, budgeted for, and waiting—no stress, no debt.

B. Replenishing and Recalculating

After the expense is paid, you do not stop the monthly contribution.

- Start Over: If the expense is annual (like insurance), you immediately recalculate the contribution based on 12 months and continue the automatic transfer to save for the next payment cycle.

- Adjust: If the expense was a one-time goal (like a wedding fund), you close that fund and reallocate that monthly contribution amount to a new Sinking Fund or boost your retirement investing.

Conclusion

Creating a Sinking Fund budget is the single best way to remove the “surprise” element from large, irregular costs. By simply identifying, calculating, and automating your savings, you bring order to financial chaos. Start today by identifying your top three most disruptive irregular expenses, performing the simple division calculation, and setting up that automatic transfer. Your future self will thank you when the next large bill arrives with zero stress.

READ MORE – Financial Sanity: Budgeting Tips for the Sandwich Generation

❓ Frequently Asked Questions (FAQ)

Q1. Can I use a Sinking Fund for an Emergency Fund?

A. No. While both involve saving, an Emergency Fund should be a one-time goal that is left untouched. Sinking Funds are designed to be spent and immediately replenished. Mixing the two makes it hard to know your true financial safety net. Keep them in separate accounts.

Q2. Where should I keep my Sinking Fund money?

A. Sinking Fund money should be kept in a High-Yield Savings Account (HYSA). This ensures the money is safe (FDIC insured), earns a small amount of interest, and remains completely liquid and separate from your day-to-day spending money.

Q3. What if I can’t afford the calculated monthly contribution?

A. If the calculated amount is too high, you have two options:

Reduce the Goal: Lower the total expense goal (e.g., choose a cheaper vacation or gift budget).

Extend the Timeline: If the due date is flexible, give yourself more time (e.g., save for 18 months instead of 12). If the due date is fixed (like car insurance), you must reduce other discretionary spending to meet that essential monthly contribution.

Q4. Should I use one account for all my Sinking Funds?

A. Yes, you can use one High-Yield Savings Account for all Sinking Funds, provided you use a clear tracking system (like a spreadsheet or your budgeting app) to track the internal “virtual” balance of each individual fund (e.g., Vacation: ₹15,000, Insurance: ₹7,000). This keeps things simple but requires discipline.

2 thoughts on “Mastering Sinking Funds: Your Step-by-Step Guide to Saving for Big Expenses”