We’ve all been there: facing an unexpected expense just before payday. Maybe the car broke down, or a medical bill arrived, and you need cash now. In this moment of urgency, two options often appear: the fast, deceptively easy Payday Loan, and the more traditional, slower Personal Loan.

While the payday loan promises immediate relief, it comes with a silent, devastating cost. It is one of the most financially damaging products available, preying on desperate circumstances. A personal loan, while requiring more planning, offers a sustainable path to solving short-term crises.

This guide is a critical comparison. We’ll strip away the confusing jargon to reveal the single, most important number you need to know—the Annual Percentage Rate (APR)—and demonstrate, with clear examples, why choosing the right financial tool is the difference between temporary relief and a long cycle of debt.

I. Defining the Financial Tools

Though both are loans, their structures and risks are fundamentally different.

A. The Payday Loan: Instant Access, Catastrophic APR

A payday loan is a short-term, high-cost, unsecured loan, typically due on your next payday (usually two to four weeks).

- How it Works: You borrow a small amount (e.g., ₹5,000 to ₹50,000) and provide the lender with a post-dated check or electronic access to your bank account for the principal plus a high flat fee.

- The Flat Fee Trap: Payday loans charge a fixed fee (e.g., ₹1,500 for every ₹10,000 borrowed). This fee is what leads to the astronomical APR.

- Target Audience: Borrowers with poor credit or no credit history who need emergency funds fast.

B. The Personal Loan: Structured Repayment, Reasonable Rates

A personal loan is an installment loan typically offered by banks, NBFCs, or credit unions. It is repaid in fixed, predictable monthly installments over a longer period (e.g., 6 months to 5 years).

- How it Works: The loan amount is determined by your credit score and income. The bank charges a fixed interest rate (APR) over the entire term.

- The Fixed Rate Advantage: The cost is transparent and predictable from Day 1.

- Target Audience: Borrowers with fair to excellent credit history seeking predictable, lower-cost financing for large expenses or debt consolidation.

II. The True Cost Revealed: APR Comparison

The single most important metric for comparing these loans is the Annual Percentage Rate (APR), which includes both the interest and any mandatory fees, expressed over a year.

C. The Payday Loan’s Hidden APR

Because the fee is charged over just two weeks, the resulting APR is astronomical.

| Scenario | Fee Structure | Equivalent APR |

| Borrowing ₹10,000 | ₹1,500 fee for 14 days | 400% APR (Approx.) |

| Borrowing ₹20,000 | ₹3,000 fee for 14 days | 391% APR (Approx.) |

- The Reality Check: You are not paying 15% interest; you are paying a fee equivalent to a 400% annual interest rate. This makes the payday loan one of the most expensive ways to borrow money in existence.

D. The Personal Loan’s Transparent APR

A standard personal loan, even for someone with average credit, offers a radically lower, fixed rate.

| Loan Scenario | Typical APR Range |

| Borrower with Excellent Credit | 10% – 14% APR |

| Borrower with Fair Credit | 18% – 25% APR |

Even at the high end (25% APR), the cost of a personal loan is dramatically lower than the 400% APR of a payday loan.

III. The Cycle of Debt: Payday Loan Risk

The primary danger of the payday loan is not the initial fee, but the subsequent renewal and rollover cycle.

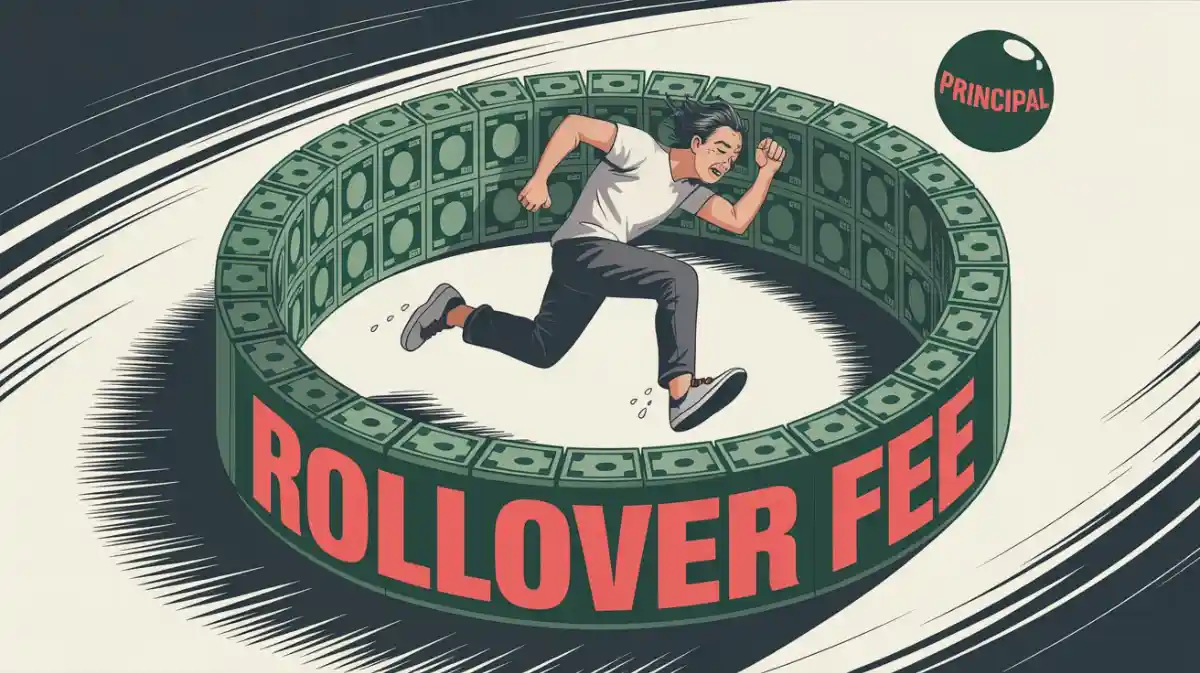

E. The Rollover Trap

Since most people cannot afford to pay the entire principal plus the hefty fee on their very next paycheck, they are forced to “rollover” the loan.

- How it Works: If you pay only the ₹1,500 fee (on a ₹10,000 loan), the ₹10,000 principal is extended for another two weeks, incurring another ₹1,500 fee.

- The Result: After three months, you might have paid ₹9,000 in fees alone, yet you still owe the original ₹10,000 principal. This traps borrowers in a never-ending cycle of fees that can quickly spiral into financial ruin.

F. The Default Risk

If you default on a payday loan, the lender immediately attempts to withdraw funds directly from your bank account. This can trigger overdraft fees from your bank, further compounding your financial distress. The combination of payday fees and bank fees is often devastating.

IV. Action Plan: How to Choose the Better Solution

Your choice should always be driven by the APR and the term structure.

G. Choose a Personal Loan When:

- You Need Time to Repay: The fixed monthly installments spread the cost over months, making the debt manageable and predictable.

- You Have Decent Credit: Even a fair credit score (650+) will qualify you for a rate significantly lower than 400% APR.

- The Total Cost is Your Priority: You prioritize paying the least amount of total interest over the life of the loan.

H. Alternatives to Payday Loans (Use These Instead!)

If a bank denies you a personal loan due to low credit, never resort to a payday loan. Consider these safer alternatives:

- Credit Union PALs (Payday Alternative Loans): Offered by credit unions, these have caps on interest and application fees, providing a much safer, regulated option.

- Borrow from Family/Friends: If possible, borrowing interest-free from your network is always the cheapest solution.

- Secured Loan: Use an asset (like gold or a fixed deposit) as collateral to get a low-rate loan, as this eliminates the need for high-risk, high-interest products.

- Negotiate with Creditors: Call the utility company or hospital and ask for a payment plan or extension. Most institutions are willing to work with you.

Conclusion

The appeal of the payday loan is instant gratification, but its cost is a financial time bomb. The 400% APR comparison is the only number that truly matters. For short-term crisis financing, you must always exhaust all possibilities for a Personal Loan or a regulated alternative. Prioritize a fixed, structured repayment plan over the deceptive speed of the payday loan, ensuring that a quick fix doesn’t become a long-term financial disaster.

❓ Frequently Asked Questions (FAQ)

Q1. Is the interest rate on a Payday Loan illegal?

A. While many consumer advocates argue they should be illegal, payday loans operate in a legal gray area. They charge a “fee” rather than “interest,” allowing them to bypass traditional interest rate caps (usury laws) set for installment loans in many regions.

Q2. Does a Personal Loan help build credit, but a Payday Loan does not?

A. Yes, this is a key difference. Since personal loans are installment loans reported to credit bureaus, consistent, timely payments build a positive credit history. Most payday lenders do not report positive payment history, meaning they do nothing to help your credit score; they only report when you default (negative history).

Q2. Does a Personal Loan help build credit, but a Payday Loan does not?

A. Yes, this is a key difference. Since personal loans are installment loans reported to credit bureaus, consistent, timely payments build a positive credit history. Most payday lenders do not report positive payment history, meaning they do nothing to help your credit score; they only report when you default (negative history).-

Q4. Are there any fees for paying off a Personal Loan early?

A. Sometimes. A personal loan may have a prepayment penalty if you pay it off significantly early, though many modern lenders have removed this penalty. Always check the loan documents for the “prepayment clause” before signing, especially if you plan to pay it off quickly.

1 thought on “The True Cost: Short-Term Payday Loan vs. Personal Loan – A Real-World Comparison”