For many graduates, the student loan is the single largest financial obligation they carry into their early working years. While education is an investment, the monthly repayment is pure debt. When applying for any major new credit—be it a mortgage, a car loan, or a large personal loan—lenders will scrutinize one metric above all others: the Debt-to-Income (DTI) Ratio.

Your DTI ratio is the lender’s primary gauge of your ability to handle new debt. It is a calculation that measures how much of your gross monthly income is consumed by debt payments. Crucially, lenders look at student loans differently than credit card or mortgage debt, making accurate calculation vital for approval.

This comprehensive guide will demystify the DTI ratio, explain exactly how to calculate it when student loan debt is a factor, and provide actionable strategies to lower your DTI to ensure you qualify for the best interest rates on your next big financial application.

I. Defining the DTI Ratio and Its Importance

A. The Simple DTI Formula

The DTI ratio is expressed as a percentage. It is calculated by dividing your total monthly debt payments by your gross monthly income (income before taxes and deductions).

The formula is:

$$\text{DTI Ratio} = \frac{\text{Total Monthly Debt Payments}}{\text{Gross Monthly Income}} \times 100$$

- Example: If your gross monthly income is ₹1,00,000 and your total monthly debt payments are ₹30,000, your DTI is 30%.

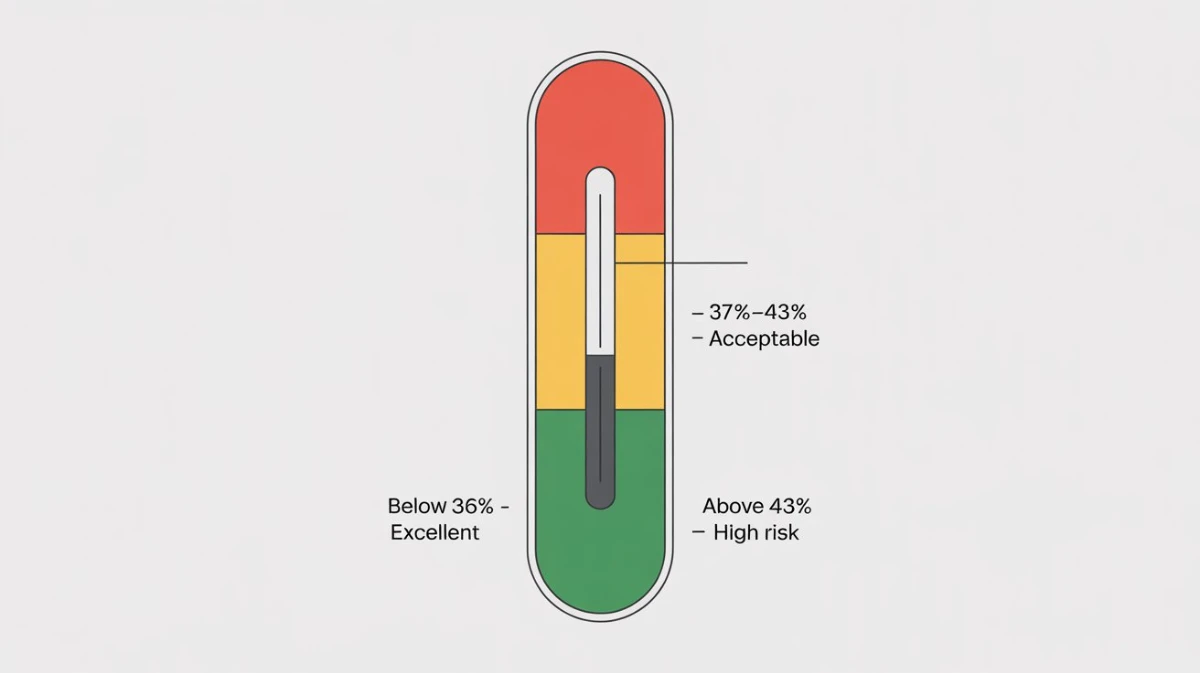

B. The Lender’s Thresholds

Lenders use DTI as a hard cutoff point. Your goal should always be to fall below the lowest possible threshold to secure premium rates.

| DTI Percentage | Risk Assessment | Implication for Borrower |

| Below 36% | Excellent | Best rates for mortgages and auto loans. |

| 37% – 43% | Acceptable | May qualify, but rates will be higher. |

| Above 43% | High Risk | Likely rejection for conventional mortgages and large loans. |

II. Phase 1: The Student Loan DTI Calculation Dilemma

This is where the calculation gets tricky, especially if you are on an income-driven repayment plan or if your loans are currently deferred.

C. The Standard DTI Calculation for Fixed Loans

If your student loan is in standard repayment with a fixed monthly payment (Principal + Interest), the calculation is straightforward:

- Simply use the actual fixed monthly payment amount shown on your statement and include it in your Total Monthly Debt Payments (the numerator).

D. Dealing with Income-Driven Repayment (IDR) Plans

IDR plans (like SAVE or PAYE in the US, or other income-linked programs) often complicate the DTI. These plans often lead to a lower monthly payment, sometimes even ₹0.

- The ₹0 Payment Trap: If your IDR plan shows a ₹0 monthly payment, some conventional lenders (especially mortgage providers) will NOT use zero. They may instead calculate your payment using 0.5% to 1.0% of the total outstanding loan balance.

- Action: If you owe ₹20,00,000, a lender might use ₹20,000 (1.0% of the balance) as your expected monthly payment, dramatically increasing your calculated DTI and potentially leading to rejection.

- The Deferment/Forbearance Issue: If your student loans are currently in deferment or forbearance (where payments are paused), the lender will usually not use a zero payment. They will likely use the same conservative 1.0% of the total balance method.

E. The DTI Optimization Strategy for Student Loans

To counter the lender’s conservative estimate (the 1.0% method), you must provide official documentation:

- Provide the Official Payment Letter: If you are on an IDR plan, provide the lender with the official documentation from your loan servicer that explicitly states your actual monthly payment amount (e.g., ₹5,000). Many lenders will accept this lower, documented payment, saving you thousands on your calculated DTI.

III. Phase 2: Actionable Strategies to Lower Your DTI

If your DTI is currently above 40%, you must actively reduce it before applying for a new loan. There are only two ways to lower DTI: increase the denominator (income) or decrease the numerator (debt payments).

F. Reducing the Numerator (Debt Payments)

This is the fastest path to DTI reduction.

- Attack Credit Card Debt: Credit cards carry no emotional value and are the highest-interest debt. Use methods like the Debt Avalanche (paying off the highest interest rate first) to quickly reduce the balances and their associated minimum payments.

- Avoid New Debt: Freeze all new credit card usage and loan applications for at least six months before applying for a major loan (like a mortgage).

- Pay Off Small Debts Entirely: Focus on clearing any small installment loans (like an old phone financing plan). Eliminating a debt entirely removes its monthly payment from the DTI calculation instantly.

G. Increasing the Denominator (Gross Income)

While harder, increasing documented income is a long-term solution.

- Document All Income: Ensure all sources of income (freelance, side-gig, commissions) are fully reported on your tax returns, as lenders will use your tax records as proof.

- Ask for a Raise: Negotiate a salary increase at your current job. A permanent increase in gross income directly and permanently lowers your DTI.

IV. Conclusion: DTI is Your Financial Gatekeeper

The Debt-to-Income ratio is the single most important metric controlling your access to future financial opportunities. For anyone burdened by student loan debt, simply using the standard calculation is not enough. You must understand how lenders conservatively calculate IDR and deferment payments. By proactively reducing your high-interest debt and securing official documentation for your lowest possible student loan payment, you control your DTI narrative, ensuring that your future financial goals remain within reach.

❓ Frequently Asked Questions (FAQ)

Q1. Is DTI the same as my Credit Score?

A. No. Your Credit Score (CIBIL/FICO) measures your past ability and willingness to pay (your history). Your DTI ratio measures your current ability to afford a new payment based on your income. Lenders use both, but DTI is often the first hurdle for major loans.

Q2. Do I use Net Income or Gross Income for the DTI calculation?

A. Always use Gross Monthly Income (income before taxes, insurance, or deductions) for the denominator. Lenders prefer this higher number because it shows your total earning power, though they factor in taxes separately later.

Q3. Do household expenses like groceries and utilities count towards DTI?

A. No. DTI only includes recurring, mandatory debt obligations that are reported on your credit file (loans, credit card minimums, and rent/mortgage payments). Regular household expenses like groceries, insurance premiums, utilities, and internet bills are typically excluded from the official DTI calculation.

Q4. Should I pay off my student loans or save for a down payment to improve DTI?

A. This is a common dilemma. If your DTI is currently high (above 40%), prioritize paying down high-interest consumer debt (credit cards) first. If your DTI is acceptable, focusing on saving for the down payment is usually better, as lenders value the low LTV (Loan-to-Value) that a large down payment provides, and paying off a fixed, low-interest student loan doesn’t significantly change your DTI proportion.