It starts with a family gathering. Your nephew, niece, or a close friend’s son has secured admission to a prestigious university abroad or a top MBA college in India. Everyone is celebrating.

Then, the request comes.

“Mama ji (Uncle), the bank just needs a guarantor. It’s a formality. Just one signature from you, and my future is set. You trust me, right?”

Of course, you trust them. You want to help. You think, “I’m not paying the money, I’m just vouching for him.” You sign the papers, eat the laddoo, and forget about it.

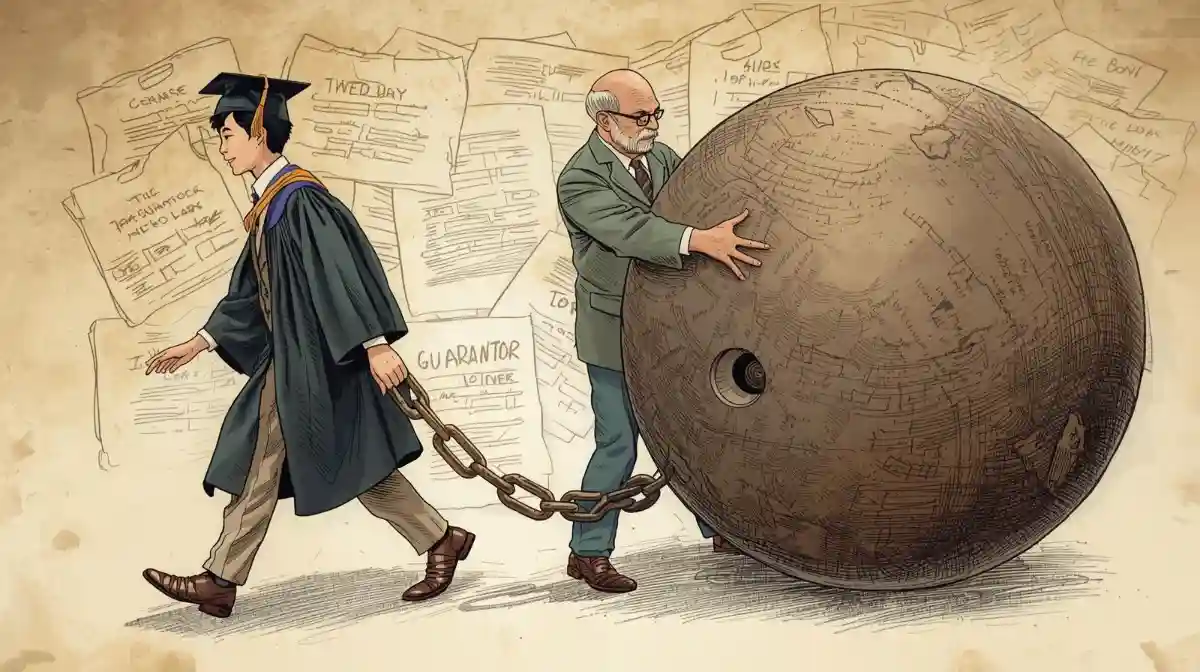

Stop. You might have just committed financial suicide.

In the eyes of the bank, you didn’t just give a character reference. You effectively said: “If he doesn’t pay, I will.”

Becoming a guarantor for an education loan (which often ranges from ₹20 Lakhs to ₹50 Lakhs) is one of the riskiest financial decisions an Indian can make. In this brutally honest guide, we will uncover the legal, financial, and credit score nightmares that hide behind that “single signature,” and why you should think ten times before agreeing.

I. Who is a Guarantor? (It’s Not Just a Reference)

Let’s clear up the biggest myth immediately. A Guarantor is NOT a Witness.

- A Witness: Someone who confirms “Yes, this person is Mr. Rahul.” They have zero financial liability.

- A Guarantor: Someone who provides a legal guarantee to the bank.

The Bank’s Logic

Banks aren’t stupid. They know that a fresh graduate might not get a job, or might settle abroad and ignore Indian debts. They need a “backup target” who has assets and a stable income in India. That target is you.

When you sign as a guarantor, you are entering a legal contract that makes you equally liable for the debt. The moment the student defaults, the bank doesn’t have to chase the student; they can come straight for you.

II. The 3 Silent Killers: How It Destroys Your Finance

Most guarantors sleep peacefully until 3 years later when their own loan application gets rejected. Here is how the damage happens.

1. The CIBIL Score Crash (The Silent Killer)

This is the most shocking realization for guarantors.

- The Scenario: The student misses 3 EMIs because he is searching for a job.

- The Impact: The bank reports this default to CIBIL. But they don’t just report it on the student’s PAN card; they report it on YOUR PAN card too.

- The Result: Your CIBIL score crashes by 50-100 points, even though you have paid all your own bills on time. You are punished for someone else’s mistake.

2. Reduced Loan Eligibility (The Debt Trap)

Imagine you want to buy a house next year. You apply for a Home Loan. The bank manager checks your profile and says, “Sir, your loan capacity is zero.”

- Why? When calculating your eligibility, banks look at your Total Liability. Even if the education loan is being paid on time by the student, the bank treats that ₹20 Lakhs as YOUR contingent liability.

- The Math: If you guarantee a ₹20 Lakh loan, the bank assumes you might have to pay it. Therefore, they deduct that EMI amount from your disposable income, drastically reducing the amount you can borrow for your own needs.

3. Asset Attachment (The Legal Nightmare)

If the education loan turns into an NPA (Non-Performing Asset) and the amount is large (e.g., ₹40 Lakhs for US/UK studies), the bank can use the SARFAESI Act or approach the Debt Recovery Tribunal (DRT).

- The Power: They have the legal right to attach (seize) your assets—your house, your fixed deposits, or your salary account—to recover the dues. They don’t have to sell the student’s assets first; they can go for whichever asset is easiest to liquidate. Often, that’s yours.

III. The “NRI Student” Risk Factor

This is a specific problem in India.

- The Situation: You sign for a student going to the USA/Canada.

- The Reality: The student moves abroad, gets a job, and changes their phone number. They stop caring about their Indian CIBIL score because they are building a credit score in the US.

- The Consequence: The Indian bank cannot easily chase the student in New York. But they know exactly where you live in Delhi or Mumbai. You become the primary target for recovery agents.

IV. Co-Borrower vs. Guarantor: Know the Difference

Often, parents are Co-borrowers, while relatives are Guarantors.

| Feature | Co-Borrower (usually Parent/Spouse) | Guarantor (Third Party/Relative) |

| Relationship | Close blood relative. | Can be uncle, friend, cousin. |

| Ownership | Often joint owner of collateral. | Usually brings additional security. |

| Liability | Primary (First in line). | Secondary (But effectively equal). |

| Benefit | Can claim tax deduction (Sec 80E). | No tax benefit whatsoever. |

Crucial Point: As a guarantor, you take 100% of the risk but get 0% of the tax benefits under Section 80E. It is a lose-lose deal for you.

V. How to Protect Yourself (If You MUST Sign)

Sometimes, you can’t say no to family. If you are forced to sign, use these safety nets.

1. Demand “Loan Insurance” (Non-Negotiable)

Make it a condition: “I will sign only if you buy a Loan Protection Insurance policy.”

- This insurance covers the loan amount if the student dies or becomes disabled. It prevents the debt from falling on your head in a tragedy.

2. Limit Your Liability

Ask the bank if you can sign a “Limited Guarantee” deed rather than an unlimited one. This limits your liability to a specific amount (e.g., ₹5 Lakhs) or a specific time period, though banks rarely agree to this for retail loans.

3. Keep Access to the Account

Insist on having Net Banking access or receiving monthly email statements for the loan account.

- Why? You need to know the moment an EMI is missed. Don’t wait for the bank to send a legal notice 6 months later. If the student misses a payment, pay it yourself immediately to save your CIBIL score, then fight with the family later.

4. The Exit Strategy

Ask the bank: “Once the student gets a job and completes 2 years of repayment, can you remove me as a guarantor?”

- Some banks allow this if the primary borrower (student) proves their salary is sufficient to carry the loan alone. Get this assurance in writing if possible.

Conclusion: Learn to Say “No”

Helping family is a virtue, but risking your financial retirement is foolishness. The best help you can give a student is to guide them towards a scholarship or a loan that doesn’t require a third-party guarantee (many banks offer this for premier institutes like IITs/IIMs).

If you must sign, go in with your eyes open. Understand that you are not just helping a student; you are signing a check that you hope will never be cashed. Protect your CIBIL score like your life depends on it—because your financial future does.

READ MORE – Why Your Mudra Loan Got Rejected: The Real Reasons Banks Won’t Tell You

⚠️ Disclaimer

Financial Disclaimer: The information provided in this article is for educational purposes regarding banking norms in India. Being a guarantor is a legal liability. The laws regarding debt recovery (SARFAESI, DRT) are complex. Please consult a legal expert or Chartered Accountant before signing any loan guarantee deed. ZunoMoney is not responsible for any legal or financial losses arising from such decisions.

❓ Frequently Asked Questions (FAQ)

Q1. Can I withdraw my name as a guarantor later?

A. It is extremely difficult. You cannot just “resign.” The bank must agree to release you, and they will only do so if the borrower provides a replacement guarantor with equal or better financial standing. If the borrower refuses to find a replacement, you are stuck until the loan is closed.

Q2. If the student dies, do I have to pay?

A. Sadly, yes. Unless there is Loan Insurance, the liability shifts to the guarantor. The debt does not die with the student. This is why insisting on insurance is crucial.

Q3. Does being a guarantor affect my Income Tax?

A. No. You do not get any tax benefits (like Section 80E deduction on interest) for being a guarantor. However, if you are forced to repay the loan, that money is gone from your taxed income, and you get no relief for it.

Q4. Can the bank take my house if I am just a guarantor?

A. Yes, if the loan amount is large and you pledged your house as collateral (or if you have significant assets). Under the SARFAESI Act, banks can auction the guarantor’s property to recover dues if the borrower fails to pay. They treat you exactly like the borrower.