The “Kiraya” (Rent) Dream

Ask your father or uncle: “What is the best way to generate monthly income for retirement?”

10 out of 10 times, the answer will be: “Beta, buy a flat or a shop. The rent will take care of you.”

In India, Real Estate is not just an investment; it is an emotion. We believe that a brick-and-mortar house is the only “safe” asset. The idea of earning ₹20,000 rent while sitting at home sounds perfect.

But have you done the math?

Did you know that to earn ₹20,000 rent, you need to buy a property worth ₹80 Lakhs to ₹1 Crore? That is a return of just 2% to 3%. Even a Savings Bank Account gives more than that!

In this eye-opening guide, we will introduce you to the Systematic Withdrawal Plan (SWP)—a smarter, modern alternative that can generate 3x more monthly income than a flat, with zero tenant headaches and lower taxes.

It’s time to break the age-old myth: Don’t buy a second home for rent. Buy freedom instead.

I. The Harsh Reality of Rental Yield in India

Let’s look at the numbers objectively.

If you buy a flat in a metro city like Mumbai, Delhi, or Bangalore for ₹50 Lakhs, how much rent can you realistically expect?

- Average Rent: ₹12,000 to ₹15,000 per month.

- Annual Rent: ₹1,80,000.

- Gross Return: (1.8L / 50L) * 100 = 3.6%.

But wait, this is “Gross” return. Now subtract the expenses:

- Maintenance: Society charges (₹2,000/month).

- Property Tax: Yearly payment to municipality.

- Repairs: Painting, plumbing leaks (at least one month’s rent goes here).

- Vacancy: The months when you don’t find a tenant (0 income).

Net Return: After expenses, your actual return drops to 2% or 2.5%. This is shockingly low compared to inflation (6%). You are actually losing purchasing power every year.

II. Enter the Challenger: What is SWP?

SWP stands for Systematic Withdrawal Plan. It is the exact opposite of an SIP.

- SIP: You put small money in to build a big corpus.

- SWP: You put a big corpus in and take small money out every month.

You invest your ₹50 Lakhs in a Hybrid Mutual Fund (Safety + Growth). You instruct the fund: “Please send ₹30,000 to my bank account on the 1st of every month.”

The remaining money stays invested and keeps growing.

III. The Battle: ₹50 Lakh Flat vs. ₹50 Lakh SWP

Let’s put them in the ring. Two friends, Ramesh (Real Estate) and Suresh (SWP), both retire with ₹50 Lakhs.

Scenario:

- Investment Amount: ₹50,00,000

- Goal: Monthly Income

| Feature | Ramesh (Buy a Flat) | Suresh (Mutual Fund SWP) |

| Asset Bought | 2BHK Flat | Hybrid/Balanced Advantage Fund |

| Monthly Income | ₹12,000 (Rent) | ₹30,000 (Fixed Withdrawal) |

| Yearly Income | ₹1.44 Lakhs | ₹3.60 Lakhs |

| Rate of Return (Yield) | ~2.5% | ~6% Withdrawal + Growth |

| Tenant Headache | High (Calls for repairs, late rent) | Zero (Automated Credit) |

| Liquidity | Very Low (Cannot sell 1 room) | Very High (Withdraw anytime) |

| Taxation | Taxed at Income Slab (Up to 30%) | Capital Gains (Much Lower) |

| Winner | ❌ | ✅ (Winner) |

The Result: Suresh is earning more than double the income of Ramesh with the same ₹50 Lakhs investment. Plus, Suresh doesn’t have to chase tenants or pay for whitewashing every Diwali.

IV. “But Property Prices Go Up!” (Capital Appreciation)

Ramesh argues: “But my flat value will double in 10 years!”

Fair point. Real Estate appreciates. But so do Mutual Funds.

- Real Estate Growth: Historically 5% – 7% in India (last 10 years).

- Equity Mutual Fund Growth: Historically 10% – 12%.

The Magic of SWP:

Even after withdrawing ₹30,000 every month from your Mutual Fund, the remaining balance continues to grow.

- Example: If the fund generates 10% returns and you withdraw 6% (SWP), your capital still grows by 4% every year.

- So, after 20 years, Suresh will have eaten monthly income AND his original ₹50 Lakhs would have grown to ₹1 Crore+.

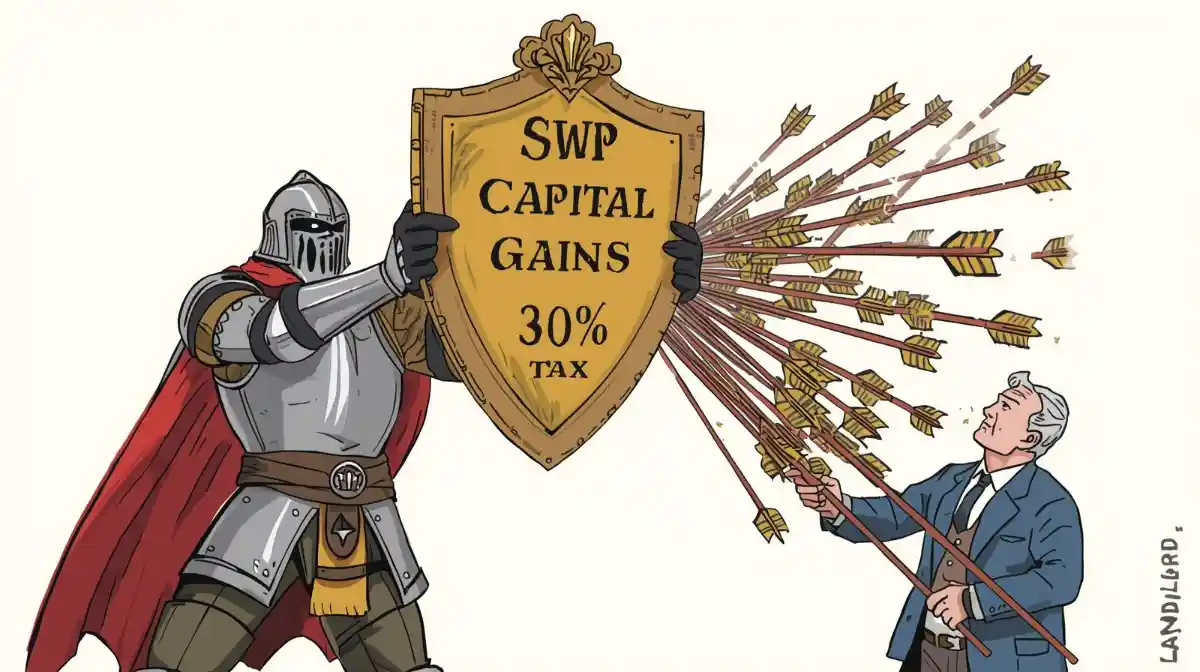

V. The Hidden Villain: Taxation

This is where SWP completely destroys Rental Income.

1. Tax on Rent

Rental income is added to your total income.

If you are in the 30% Tax Bracket:

- You earn ₹15,000 rent.

- You pay ₹4,500 tax.

- In hand: ₹10,500.

2. Tax on SWP (The Loophole)

In SWP, you are technically “selling units.” The money you receive is a mix of your own Principal (Not Taxed) and Capital Gains.

- For the first few years, the “Gain” part in your withdrawal is very small.

- Result: You pay almost ZERO tax on SWP income for the first 3-5 years. Even later, it is taxed at only 12.5% (LTCG) and that too only on the profit part exceeding ₹1.25 Lakhs.

Verdict: SWP is practically tax-free monthly income for many retirees.

VI. The Risks: Is SWP Safe?

Real Estate feels safe because you can touch it. Mutual Funds feel risky because they fluctuate.

How to make SWP safe?

Don’t put all ₹50 Lakhs in high-risk Small Cap funds.

- Use Conservative Hybrid Funds or Balanced Advantage Funds.

- These funds invest 30-60% in Debt (Bonds/FDs) and the rest in Stocks.

- They provide the stability of FD and the growth of Equity. They don’t crash hard when the market falls.

VII. Action Plan: How to Set Up Your Own Pension

If you have a lump sum amount (from retirement, property sale, or inheritance):

- Don’t rush to buy property. Stop and calculate the rental yield in your area. If it is below 3%, walk away.

- Select the Right Fund: Choose a “Balanced Advantage Fund” (e.g., HDFC, ICICI, or SBI Balanced Advantage).

- Start SWP: Go to the AMC website, select “SWP”.

- The Golden Rule: Withdraw only 6% of your total corpus annually.

- If you have ₹50 Lakhs, withdraw ₹3 Lakhs/year (₹25,000/month).

- This ensures your money never runs out and keeps growing to beat inflation.

Conclusion: Be a Modern Landlord

Being a landlord is stressful. Being an investor is peaceful.

The days of blindly buying property for pension are over. The math simply doesn’t support it anymore in India.

Switch to SWP. Let the top companies of India pay your monthly “Rent,” while you sit back and enjoy your tea without worrying about a leaking tap or a tenant refusing to vacate.

READ MORE – The “Zero Brokerage” Lie: 7 Hidden Demat Charges & Safety Risks

⚠️ Disclaimer

Financial Disclaimer: Mutual Fund investments are subject to market risks. The example of ₹50 Lakhs and 10-12% returns is based on historical data of Hybrid Funds and is not a guarantee of future performance. Real Estate returns vary by location. Please consult a SEBI Registered Investment Advisor (RIA) before setting up an SWP for retirement.

❓ Frequently Asked Questions (FAQ)

Q1. Can I stop or change the SWP amount later?

A. Yes, anytime. SWP is fully flexible. If you want to increase the monthly amount from ₹20k to ₹25k, or stop it for a few months, you can do it with a single click. You cannot do this with Rent (you can’t ask a tenant for a hike every month!).

Q2. What if the market crashes? Will my SWP stop?

A. No, the SWP continues. The fund will sell more units to give you the fixed amount. However, this can reduce your capital. Solution: That is why we recommend “Balanced Advantage Funds” or keeping 3 years of income in a Debt Fund to protect against crashes.

Q3. Is Rental Income ever better than SWP?

A. Yes, in one specific case: Commercial Real Estate. If you own a shop or office space, the rental yield can be 6-8%, which is comparable to SWP. But Residential property (flats) almost never beat SWP.

Q4. Is SWP taxable for Senior Citizens?

A. Yes, but it is highly tax-efficient. Up to ₹1.25 Lakhs of Capital Gains (profit) per year is tax-free. Since a large part of your SWP is just your own principal coming back, you effectively pay very little tax compared to FD interest or Rent.