Introduction: Is Your Money Sleeping or Working?

Let’s be honest about your Savings Account. It’s convenient, it’s safe, but as an investment? It’s terrible.

In India, most standard savings accounts offer an interest rate of 3% to 3.5%. Meanwhile, inflation is hovering around 6%. Do the math: if your money is sitting in a standard savings account, it is actually losing value every single day. It’s “lazy money.”

But what if I told you there is a switch you can flip? A hidden feature that forces your same boring savings account to pay you Fixed Deposit (FD) interest rates (up to 7%), without locking your money away for years?

This feature is called the Auto-Sweep Facility (also known as Savings Plus, Money Multiplier, or 2-in-1 Account). Banks don’t advertise it aggressively because it costs them money. They prefer you to keep your funds at 3% so they can lend it out at 10%.

In this comprehensive guide, we are going to expose how this facility works, do the math on how much extra you can earn, and walk you through the fine print so you can stop letting inflation eat your savings.

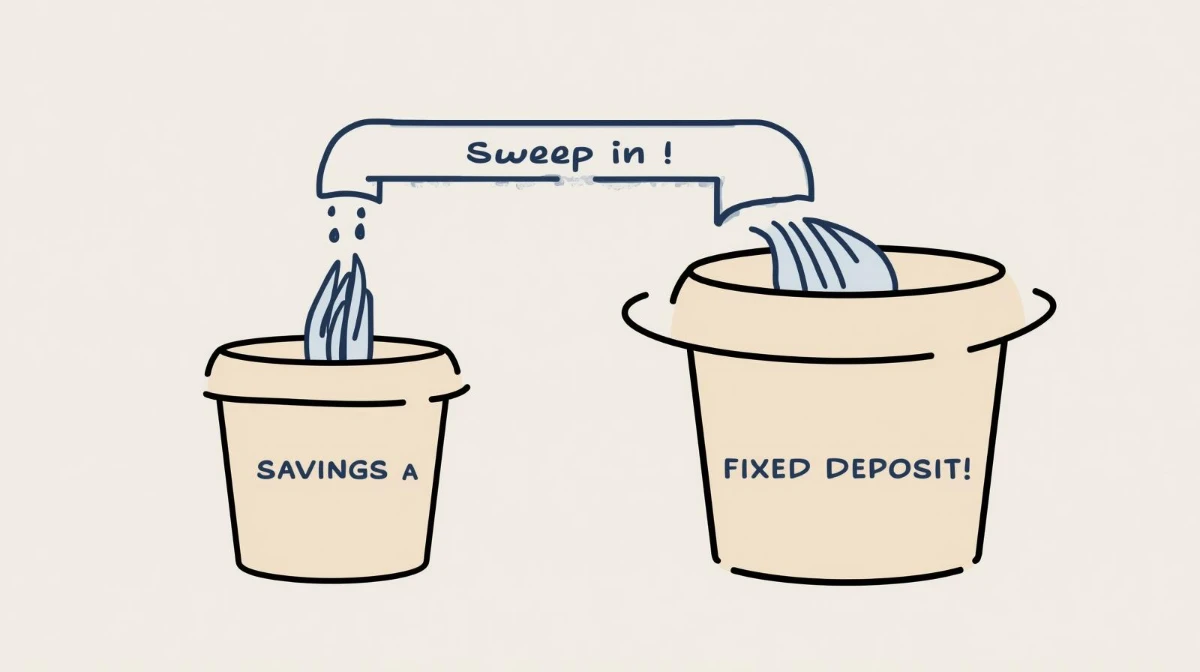

I. What Exactly is the Auto-Sweep Facility?

Think of the Auto-Sweep facility as a bridge between your Savings Account and a Fixed Deposit (FD).

Normally, you have to choose:

- Savings Account: High liquidity (money anytime), low returns.

- Fixed Deposit: High returns, low liquidity (money locked).

Auto-Sweep gives you the best of both worlds. It automatically moves (sweeps) idle money from your savings account into an FD to earn higher interest. But—and this is the magic part—if you need to spend that money, it automatically moves it back (reverse sweeps) into your savings account instantly.

The “Bucket” Analogy

Imagine you have two buckets:

- Bucket A (Small): Your active Savings Account.

- Bucket B (Large): Your high-interest FD.

When Bucket A gets too full (exceeds a limit you set), the extra water spills over into Bucket B to earn more. When Bucket A gets empty (you spend money), water flows back from Bucket B to fill it up. You never have to manually pour the water; the system does it for you.

II. How It Works: The Mechanics of “Sweep-In” and “Sweep-Out”

To use this effectively, you need to understand two critical numbers: the Threshold Limit and the Minimum Balance.

1. The Threshold Limit (The Trigger)

This is the limit you set. Any money above this amount gets swept into an FD.

- Example: You set a threshold of ₹25,000.

- You deposit ₹1,00,000 into your account.

- The bank keeps ₹25,000 in the savings account (earning 3%).

- The remaining ₹75,000 is automatically turned into an FD (earning 6.5% or 7%).

2. The Reverse Sweep (The Safety Net)

Now, imagine you need to pay a rent of ₹40,000.

- You only have ₹25,000 in your savings “bucket.”

- You issue the check or make the UPI payment for ₹40,000.

- The bank automatically “breaks” ₹15,000 worth of your FD, moves it to savings, and clears the payment.

- Result: The payment succeeds, and you didn’t pay any penalty. The remaining ₹60,000 in the FD continues to earn high interest.

III. The Real Calculation: How Much More Do You Earn?

Let’s look at a real-world scenario to see if the hassle is worth it.

Scenario: You maintain an average balance of ₹2,00,000 in your account for one year.

- Threshold Limit: ₹25,000.

- Savings Rate: 3%

- FD Rate: 6%

Option A: Normal Savings Account

- Interest on ₹2,00,000 @ 3% = ₹6,000

Option B: Auto-Sweep Account

- First ₹25,000 stays in Savings @ 3% = ₹750

- Remaining ₹1,75,000 goes to FD @ 6% = ₹10,500

- Total Interest: ₹11,250

The Difference: You earned ₹5,250 extra just by enabling a feature. That is nearly double the return for zero extra effort. Over 5 or 10 years, this difference becomes massive due to compounding.

IV. The Fine Print: What Banks Don’t Tell You (The Catches)

This sounds perfect, right? It is, but only if you navigate the rules carefully. Banks add certain conditions that can reduce your earnings if you aren’t careful.

A. LIFO vs. FIFO (The Interest Trap)

When the system breaks your FD to pay for an expense, which FD does it break?

- FIFO (First In, First Out): It breaks the oldest FD first. This is bad because that FD has accumulated the most interest time.

- LIFO (Last In, First Out): It breaks the newest FD first. This is better. It preserves your older FDs that are close to maturity.

- Action: Ask your bank which method they use. SBI typically uses LIFO (good), while some private banks use FIFO.

B. The Minimum Tenure Condition

For an FD to earn interest, it usually needs to exist for a minimum of 7 to 30 days (depending on the bank).

- If money is swept into an FD on Monday and you spend it on Wednesday (3 days later), you might earn 0% interest on that swept amount. Auto-sweep works best for money that sits idle for at least a month.

C. Pre-Mature Penalty

While most Auto-Sweep accounts claim “no penalty” for liquidity, this usually means no fee. However, you might lose the interest rate.

- Example: If you break a 1-year FD after 4 months, the bank will pay you the interest rate applicable for 4 months (e.g., 4% instead of 6%), sometimes minus a 0.5% penalty.

V. Who Should Use Auto-Sweep? (And Who Shouldn’t)

Auto-sweep isn’t for everyone.

✅ Use it if:

- You keep large buffers: You always have ₹50,000+ sitting in your savings account “just in case.”

- You are saving for a short-term goal: You need the money in 3-6 months for a down payment or wedding and don’t want to lock it in a manual FD.

- You are a freelancer/business owner: Your income is irregular, so you can’t commit to a Recurring Deposit (RD).

❌ Avoid it if:

- You live paycheck to paycheck: If your balance hits zero every month end, the money won’t stay in the FD long enough (7-30 days) to earn interest.

- You have high transaction volume: If you do 100 UPI transactions a day, the constant sweeping in and out creates a messy bank statement that is a nightmare to reconcile.

VI. How to Activate Auto-Sweep (Indian Banks Guide)

Most banks do not enable this by default. You have to ask for it.

State Bank of India (SBI)

- Feature Name: Savings Plus Account.

- Activation: Can be done via Net Banking (e-Services > More > Auto Sweep) or by visiting the branch.

- Threshold: Typically ₹35,000.

HDFC Bank

- Feature Name: MoneyMaximizer or Sweep-In Facility.

- Activation: Usually requires a visit to the branch or a specific request form via Net Banking.

- Note: HDFC often links this to a dedicated FD booking rather than fully automatic sweeping for all savings accounts. Check your specific account variant.

ICICI Bank

- Feature Name: Money Multiplier.

- Activation: Can be toggled on via the iMobile app or Net Banking.

VII. Tax Implications: The Important Warning

This is where many people get confused.

Interest earned from Auto-Sweep FDs is treated as Interest from Fixed Deposits, NOT Interest from Savings Accounts.

- TDS (Tax Deducted at Source): If your total interest income from FDs (including Auto-Sweep) exceeds ₹40,000 in a financial year (₹50,000 for senior citizens), the bank will deduct 10% TDS.

- Tax Slab: The interest you earn is added to your total income and taxed according to your income tax slab.

- Comparison: Savings Account interest is tax-free up to ₹10,000 (under Section 80TTA). FD interest does not get this specific deduction (though it falls under general income).

Despite the tax, the significantly higher interest rate (6-7% vs 3%) usually makes Auto-Sweep profitable even after paying taxes.

Conclusion: Wake Up Your Money

Leaving large sums of money in a standard savings account is a financial sin. It serves the bank, not you. The Auto-Sweep facility is the ultimate tool for the “lazy investor”—it offers the safety and liquidity of a savings account with the returns of a Fixed Deposit.

Check your bank’s website or app today. If you have more than ₹25,000 sitting idle, turn on Auto-Sweep. It takes five minutes to set up, but it will pay you dividends for years to come. Stop letting inflation win; make your savings work as hard as you do.

- Disclaimer: This article is for informational purposes only and does not constitute financial advice. Interest rates and bank policies change frequently. Please consult your bank branch for the most current details before making decisions.

❓ Frequently Asked Questions (FAQ)

Q1. Is my money locked in Auto-Sweep? Can I withdraw it anytime?

A. No, your money is never locked. That is the biggest benefit. You can withdraw 100% of your funds via ATM, UPI, or cheque instantly. The system automatically breaks the necessary FD amount to honor your withdrawal. You don’t need to manually close the FD.

Q2. Does Auto-Sweep affect my EMI payments?

A. No. If you have an EMI due, the system treats it just like a withdrawal. If your savings balance is low, the Auto-Sweep will break an FD to ensure the EMI doesn’t bounce. It offers excellent protection against bounced check fees.

Q3. Why doesn’t my bank manager tell me about this?

A. Banks operate on the “Net Interest Margin”—the difference between the interest they pay you and the interest they charge borrowers. If they pay you 3% (Savings) and lend at 10%, their margin is 7%. If they pay you 6% (Auto-Sweep) and lend at 10%, their margin drops to 4%. It is more profitable for them if you don’t use Auto-Sweep.

Q4. Can I use Auto-Sweep with a Zero Balance Account?

A. Usually, no. Auto-Sweep facilities are typically premium features reserved for standard savings accounts that maintain a Minimum Average Balance (MAB), often ranging from ₹10,000 to ₹25,000 depending on the bank.