The Digital Heart Attack

It has happened to every Indian with a smartphone.

You are at a busy petrol pump or standing at a local Kirana store. You scan the QR code for ₹500, enter your PIN, and wait for the “Green Tick.” Instead, your screen flashes red: “Transaction Failed.”

But then, the dreaded SMS arrives: “Dear Customer, A/c XXXXX has been debited for ₹500.”

The shopkeeper shakes his head, “Bhaiya, paise nahi aaye” (Brother, money didn’t come). You show him the SMS. He points to his machine. An awkward standoff begins. You end up paying cash and leaving, wondering if your digital money is gone forever.

Most people just wait and pray for the refund. But did you know that if your bank delays the refund, they owe you money? According to specific RBI Guidelines, you are entitled to a compensation of ₹100 per day for the delay.

In this guide, we will cut through the panic. We will explain why UPI fails, the “T+1” refund rule, and the exact steps to claim your compensation if the bank sleeps on your money.

I. Why Does Money Get Cut if the Transaction Failed?

To solve the problem, you must understand the glitch. UPI isn’t magic; it’s a chain of digital handshakes between four parties:

- Your App (GPay, PhonePe, Paytm)

- Your Bank (Sender)

- NPCI (The central server)

- Receiver’s Bank (Shopkeeper)

The Limbo State: Sometimes, your bank successfully sends the money out (Debit), but the NPCI server blinks, or the Receiver’s bank is down. The money leaves your account but doesn’t reach the destination. It gets stuck in the digital pipeline. This is technically called a “Deemed Approved” transaction in banking terms.

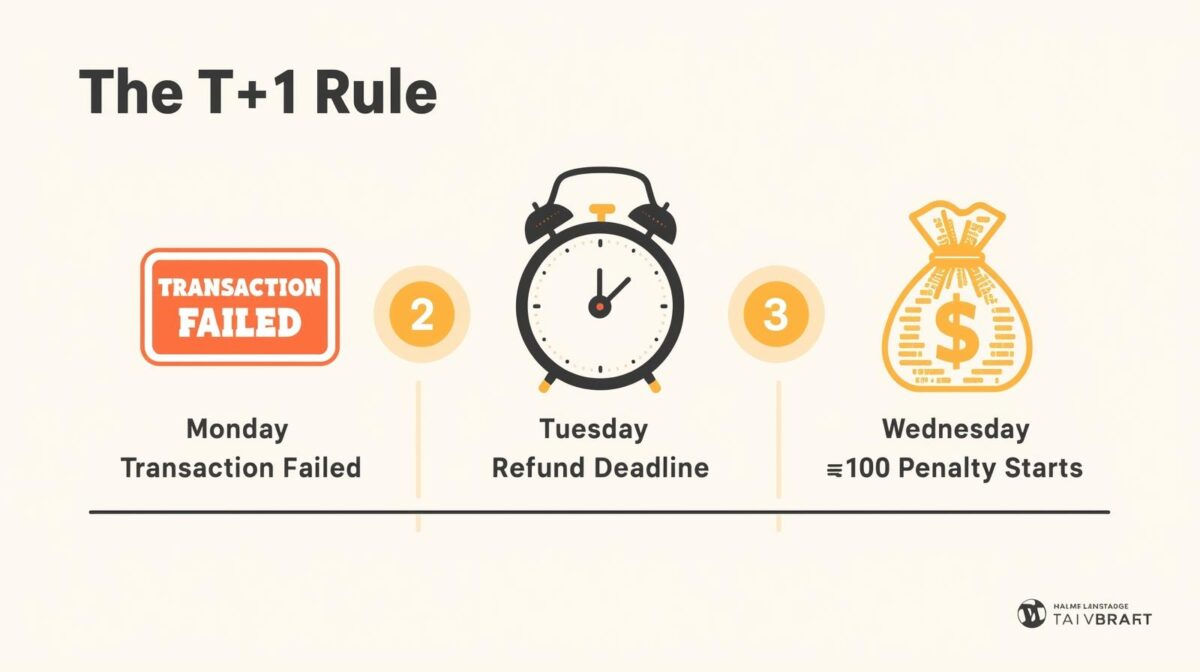

II. The RBI’s “T+1” Rule: Your Financial Rights

In 2019, the Reserve Bank of India (RBI) issued a strict circular on “Harmonisation of Turn Around Time (TAT)” for failed transactions. This is your weapon.

The Golden Rule

If money is debited from your account but not credited to the beneficiary (receiver), the bank MUST auto-reverse the money to you within T+1 days.

- ‘T’ = The day of the transaction.

- ‘+1’ = The next working day.

The Penalty Clause

If the bank fails to reverse the money by the end of T+1, they must pay you a penalty of ₹100 for every day of delay.

- Example Scenario:

- Monday: Transaction fails (Money cut).

- Tuesday: Deadline for refund (T+1).

- Friday: You finally get the refund.

- Result: The bank is 3 days late (Wed, Thu, Fri). They owe you the refund amount PLUS ₹300 compensation.

III. Action Plan: Step-by-Step Recovery Process

Don’t just wait. Follow this hierarchy to get your money back fast.

Step 1: The “1-Hour” Wait (Don’t Panic Yet)

Often, UPI failures are due to server timeouts. In 60% of cases, the status automatically updates from “Pending” to “Failed” within 1 hour, and the money is instantly reversed.

- Action: Do not pay the shopkeeper cash immediately if the app says “Processing.” Wait 10 minutes if possible.

Step 2: Raise a Dispute in the App (Mandatory)

If the money isn’t back after 1 hour, you must formally tell the system.

- PhonePe/GPay: Go to History > Select Transaction > Click “Contact Support” or “Raise Dispute.”

- Why: This logs an official ticket with the NPCI. Without this ticket, you cannot claim compensation later.

Step 3: Check UDIR (The New Tech)

The NPCI has launched UDIR (Unified Dispute and Issue Resolution).

- Most apps now check the transaction status directly with the bank’s server in real-time. If you click “Check Status,” the UDIR system often forces the reversal instantly without human intervention.

Step 4: The Ombudsman Escalation (For the Penalty)

If 3-4 days pass and you still don’t have your money (or the ₹100 penalty), send an email to your bank’s Nodal Officer or Grievance Redressal Officer.

- Subject: Failure to reverse UPI transaction – Claiming RBI Penalty.

- Content: Attach the Transaction ID and quote the “RBI Circular DPSS.CO.PD No.629/02.01.014/2019-20.”

IV. Common Myths vs. Reality

Myth: “I should call the shopkeeper’s bank.” Reality: No. You are the customer of your bank. It is your bank’s responsibility to chase the money. Don’t fight with the shopkeeper; he is innocent.

Myth: “The money is lost forever.” Reality: UPI is extremely secure. Money is never “lost.” It is either with Bank A or Bank B. It will come back; the only question is when.

Myth: “I can claim ₹100 penalty for every failed transaction.” Reality: No. You can only claim the penalty if the money was deducted and not returned within 24 hours (T+1). If the transaction failed and money wasn’t deducted, there is no penalty.

Conclusion: Know Your Rights

Digital India is fantastic, but technology isn’t perfect. The next time a server glitch eats your ₹2,000, don’t feel helpless. You have the RBI on your side. Take a screenshot, raise a dispute ticket immediately, and mark the date on your calendar. If the bank is lazy with your refund, their laziness becomes your profit. Stay calm, and let the system (and the penalty clause) work for you.

Frequently Asked Questions (FAQ)

Q1. Does the ₹100 penalty apply to Paytm Wallet or just UPI?

A. The RBI circular covers IMPS, UPI, and Wallet transactions. If money is debited from your wallet/account and not credited to the receiver, the T+1 reversal rule applies to all digital payments.

Q2. How is the penalty amount credited?

A. The bank should credit it automatically to your savings account without you asking. However, banks often ignore this. You usually have to send an email or file a complaint with the Banking Ombudsman to force them to pay the penalty.

Q3. What if the money reached the shopkeeper but he says no?

A. This is a different issue. If your app says “Success” and the money is credited to the receiver, but he denies it, you need to provide him the UTR Number (12-digit reference ID). Ask him to check his bank statement for that specific UTR number.

Q4. Where can I file a complaint if the bank ignores me?

A. If your bank does not resolve the issue within 30 days, you can file a complaint directly with the RBI Ombudsman at cms.rbi.org.in. This is a powerful tool, and banks take these complaints very seriously.